A two-week conditional ceasefire between the U.S. and Iran has forced a rapid rewrite of the Strait of Hormuz trade, but it has not fully restored the pre-war macro backdrop.

Oil has fallen sharply from the panic highs, global equities have rallied, and Bitcoin has rebounded with them. That is a clear break from the pre-ceasefire view that markets were giving up on any near-term reopening.

What has changed is the headline path for energy. What remains unresolved is the normalization path for physical flows, insurance, shipping, and inflation.

The market no longer has to price an immediate worst-case closure, but it still has to price a slower return to normal energy flows. That matters beyond oil traders because sticky fuel costs can keep inflation firmer, narrow the Fed’s room to ease, and leave Bitcoin trading as a macro risk asset rather than a clean safe-haven bet.

JPMorgan, UBS, and U.S. government energy forecasters are still describing a slower repair process beneath the ceasefire headline. Their research no longer reads as a live argument against any reopening at all. It reads as a warning that reopening and normalization are different things.

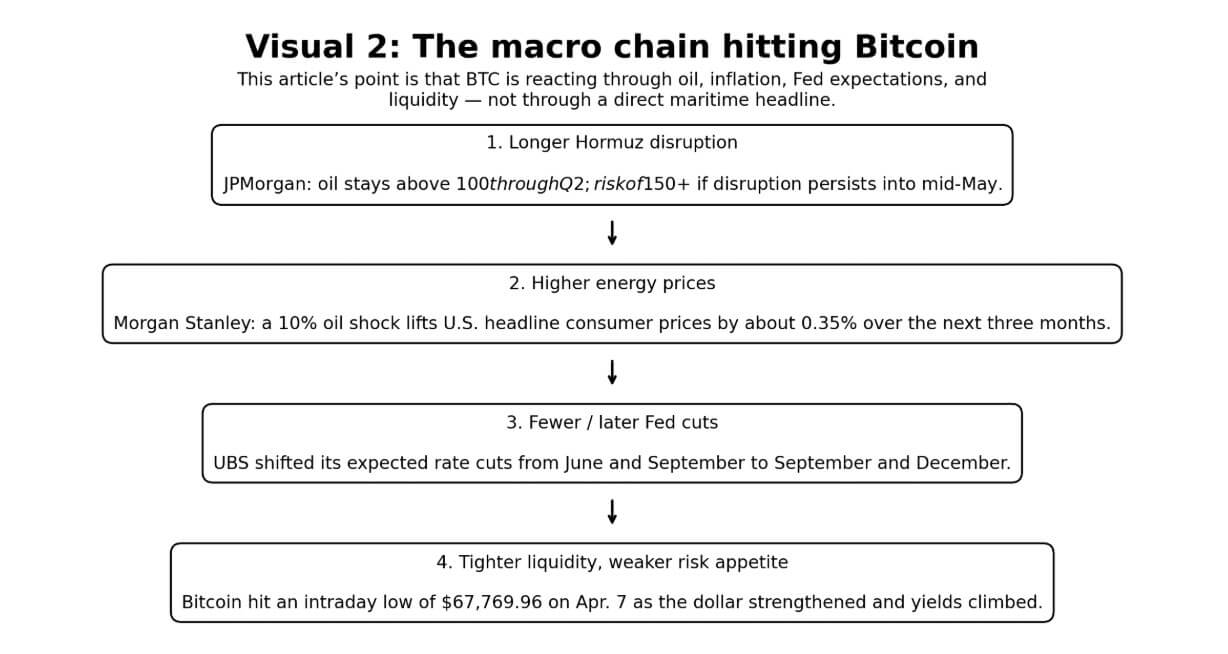

JPMorgan’s base case still keeps oil elevated through the second quarter and warns that crude could top $150 if disruptions re-escalate or persist into mid-May.

UBS expects the conflict to wind down , but says infrastructure damage means restoring production to pre-conflict levels will take considerably longer.

The EIA says that full restoration of oil flows through the Strait of Hormuz , even when the conflict concludes.

None of those three institutions is describing a full snapback in energy-market plumbing, and that is now the central point for markets. The ceasefire has reduced immediate tail risk. It has not yet guaranteed normal cargo movement, normal inventories, or normal inflation pass-through.

The Strait of Hormuz carried 20.9 million barrels per day in the first half of 2025, equal to about 20% of global petroleum liquids consumption and one quarter of all seaborne oil trade. It also handled 11.4 billion cubic feet per day of LNG, more than 20% of global LNG trade.

U.S. intelligence assessed on April 3 that Iran showed on the strait, because control over global energy flows is Tehran’s primary card.

That assessment mattered more before the ceasefire than it does now as a directional market call, but it still matters as a structural reminder that formal de-escalation does not automatically produce free navigation without friction.

Institution / actorCurrent timeline / base caseKey forecast / assessmentWhat it implies for oilWhat it implies for marketsJPMorganCeasefire lowers immediate tail risk, but disruption risk extends through Q2; partial normalization remains the base pathOil can stay elevated through Q2 and could top $150 again if disruption persists into mid-May or the ceasefire failsCrude can fall from panic highs without returning quickly to pre-shock pricingRelief rally now, but inflation and rate-cut pressure can lingerUBSConflict may cool in coming weeks, but recovery lasts longerInfrastructure damage means restoring production to pre-conflict levels takes considerably longerEnergy markets loosen before they normalizeRisk assets recover first, macro normalization follows later if at allEIAFull restoration takes months even after conflict endsFlows, routes, and output normalize slowly; retail fuel pain lingersOil and fuel prices can stay elevated after a nominal reopeningConsumer-price pressure lasts beyond the ceasefire headlineU.S. intelligenceIran still sees chokepoint control as strategic leverageTehran views energy-flow control as a core bargaining leverLower confidence in a frictionless reopeningMarkets retain a geopolitical risk premium beneath the relief moveCeasefire backdropImmediate escalation risk has eased, but durability remains unprovenMarkets can price reopening faster than shipping systems can normalizeCrude loses the panic premium first; physical tightness can linger longerRelief rally in risk assets is justified, but the macro all-clear is not yet confirmed

Physical oil markets are still the place to watch for whether reopening becomes normalization. The ceasefire has eased the headline shock, but prompt cargo pricing, insurance terms, and routing friction remain more informative than front-month futures alone.

Earlier this week, North Sea Forties crude hit $146.09 per barrel, Dated Brent reached $141.365, and some prompt cargoes traded above $150, while European jet fuel hit $226.40 and diesel $203.59. Brent futures were near $110 at the peak of the panic.

That gap between prompt physical and the headline futures screen is still where the inflation transmission lives.

In Morgan Stanley’s consumer math, a 10% rise in oil prices from a supply shock lifts U.S. headline consumer prices by roughly 0.35% over the next three months, with real consumption starting to and staying depressed for the following five to six months.

The EIA’s April outlook puts U.S. gasoline and averaging above $3.70 for 2026, with diesel peaking above $5.80 and averaging $4.80 for the year.

The macro chain

Bitcoin’s trade still goes through oil, then inflation, then Fed policy, then risk appetite. The difference after the ceasefire is that the chain has loosened. It has not broken.

Bitcoin reached an intraday low at $67,769.96 on April 7, when the oil shock, firmer dollar, and higher Treasury yields compressed risk appetite across markets.

Since the ceasefire, BTC has rebounded alongside equities as traders price a lower probability of an immediate worst-case energy spiral. That move makes sense. It does not yet settle the next question, which is whether lower oil headlines translate into a durable easing in inflation pressure and rate expectations.

Earlier this year, BTC snapped back above $70,000 as , the same logic now running again. For now, liquidity conditions, and liquidity conditions are still pricing energy.

UBS pushed its Fed rate cut expectations from June and September . raised its probability of a U.S. . IMF chief Kristalina Georgieva said that even a swift resolution would lead and higher inflation forecasts.

Dallas Fed economists of the Strait of Hormuz as lifting average WTI to $98 in the second quarter and cutting annualized global real GDP growth by 2.9% that quarter. A two-quarter disruption pushes WTI to $115 in the third quarter, and a three-quarter disruption brings it to $132 by year-end.

That modeling now works best as a risk map for ceasefire failure or incomplete normalization rather than as the live base case. The market has stepped back from the pure closure scenario. It has not yet priced a full return to pre-conflict macro conditions.

As a result, the rate-cut question has shifted. Traders are no longer asking whether the oil shock is still intensifying. They are asking whether the relief move lasts long enough to reopen Fed room later this year.

When gasoline averages above $3.70 and diesel averages above $4.80, the spending hit runs through every sector of the real economy, and financial conditions tighten well before the Fed formally acts.

Likely scenarios

The base case has changed. It is no longer outright market surrender on a near-term reopening. It is a ceasefire relief rally with incomplete normalization underneath it.

That middle path still matters for Bitcoin because lower oil is helpful only if it keeps feeding through into lower inflation pressure, steadier growth expectations, and a more credible rate-cut path.

The bear case now runs through ceasefire failure or a prolonged period where shipping resumes only partially and the physical market keeps pricing scarcity. If disruptions hold into JPMorgan’s mid-May threshold, the returns to the front of the market.

Dallas Fed modeling shows WTI hitting $115 in the third quarter under a two-quarter closure. Morgan Stanley warns that if Iran retains structural control over cargo flows even in a nominal reopening, oil markets can keep trading a higher risk premium.

For Bitcoin, that setup still maps to the clearest near-term path lower: oil stays elevated, inflation expectations grind higher, the Fed stays cautious, and risk assets lose the relief bid.

Options demand clustered around $60,000 to $50,000 downside strikes during the last acute risk-off episode. A retest of that range becomes more plausible again if the configuration deteriorates back toward the pre-ceasefire stress path.

ScenarioOil outcomeInflation effectFed implicationBTC implicationKey condition to watchBear case: ceasefire fails or disruption lasts into mid-May or longerOil re-anchors at very elevated levels; $150 returns as a working risk benchmarkInflation expectations resume grinding higherFed stays on hold longer; rate-cut hopes fade againStrongest near-term downside case; retest of lower ranges becomes more plausibleWhether disruption persists through JPMorgan’s mid-May threshold or the truce breaks downBull case: ceasefire holds and navigation normalizes genuinelyBrent falls sharply toward pre-shock levelsInflation shock unwinds fasterEasing expectations return more clearlyBTC rebounds alongside equities and broader risk assetsWhether navigation is restored freely, with insurance and cargo flows normalizing quicklyMiddle case: reopening without normalizationOil falls from extremes but retains a meaningful risk premiumInflation cools only slowlyFed gets limited relief and stays cautiousBTC improves only partially; upside remains capped by sticky macro pressureWhether reopening actually normalizes flows, inventories, and pricingSticky-aftershock casePhysical flows improve, but fuel and supply-route normalization take monthsConsumer-price pressure lingers even after calmer headlinesFinancial conditions remain tight before the Fed changes policyBTC does not get an instant all-clear even after calmer headlinesWhether gasoline, diesel, and supply-chain stress stay elevated into later quarters

The bull case is still tied to Morgan Stanley’s view that if flows return genuinely and freely, Brent could fall toward $70, as global oil had looked oversupplied before the conflict began.

In that setup, the inflation shock reverses more quickly, Fed easing returns to view, and Bitcoin recovers alongside equities. That is the logic the current relief rally is trying to price.

The condition remains decisive: genuine freedom of navigation is the requirement.

A ceasefire that leaves physical cargo movement constrained by security risk, insurance friction, congestion, or operational control produces a different oil market, where part of the risk premium stays embedded and Bitcoin’s path higher remains capped by the same inflation headwind.

That distinction between reopening and normalization is where the institutional research now converges.

The EIA says full restoration of flows will take months, even when the war ends, as supply routes and output normalize. Morgan Stanley says real consumption stays depressed for five to six months after an oil shock of this scale.

For Bitcoin traders, the relevant question is no longer whether markets believe in any reopening at all. It is whether the oil-and-inflation overhang cools fast enough to restore rate-cut expectations before the ceasefire premium fades.

Be the first to comment